There is no GOOD hidden fee in your self-funded healthcare plan.

We’re all familiar with hidden fees or undisclosed costs. We see the “extra charges” once we’re ready to check out on Ticketmaster, VRBO or any major airline, to name a few. These charges are so common that they really aren’t “hidden” anymore. We know they are coming.

We’re all familiar with hidden fees or undisclosed costs. We see the “extra charges” once we’re ready to check out on Ticketmaster, VRBO or any major airline, to name a few. These charges are so common that they really aren’t “hidden” anymore. We know they are coming.

Unfortunately, such fees in self-funded healthcare plans aren’t as easy to spot – and they can add up to significant dollars for both the self-funded employer and plan beneficiaries. Read more to learn what you should watch for in your plan agreement.

Expected Fees

The fees that self-funded employers typically monitor are administrative fees. These fees may be based on a percentage of total paid claims, or they may be calculated by a formula outlined in a plan agreement. No matter how calculated, you know these fees are a cost of having a third-party administrator (TPA) oversee your health plan operations.

Undisclosed Fees and Costs

These fees are the ones you don’t see coming. A large employer recently filed a lawsuit against its health plan administrator claiming that the TPA has, for over a decade, wrongfully charged millions of dollars in undisclosed fees. Some of the claims made in the lawsuit could be summarized as follows:

- Lack of due diligence. While timely payment of claims is expected and desired, when claims are paid “almost immediately, with no follow-up inquiry” mistakes are often made. These may be duplicate payments or overpayments. Either way, the self-funded employer is incurring costs that are not expected or justified.

- Cross-plan offsetting. If a claim is overpaid to a provider using funds from one client, it is alleged that a major TPA “corrects” this by deducting the overpayment from its next payment to the provider. While the net effect to the provider is appropriate reimbursement for services rendered, that next payment reduction is allegedly done without regard to which employer gets the benefit of the lower payment. These dollars should be credited to the employer that was charged the original overpayment.

- Use of repricing companies. When a TPA receives claims from out-of-network providers, it often engages a repricing company to negotiate lower payments to the provider. This practice should be outlined in the plan agreement and there should be transparency as to the repricing company used. In this litigation, the employer claims the TPA owns the company collecting payments for negotiating settlement amounts – an undisclosed conflict of interest and possible double-dipping.

Ways to Avoid Hidden Fees and Excess Costs

The most important thing you can do to avoid hidden or undisclosed fees in your employee health benefit plan is to ensure that you understand exactly what is in your plan agreement. When it is time to review and renew a plan agreement, consider the following:

- Fees may vary depending on the TPA and the type of policy.

- The fees may be waived or reduced under certain circumstances.

- Ask about all fees upfront, including any arrangements with companies affiliated with your TPA. Don’t be afraid to ask that all fees be disclosed and fully explained.

- Get quotes from multiple plan administrators. This is the best way to make sure that you’re getting the best deal.

- Monitor and evaluate all charges or “cost savings fees” by your TPA under any “shared” cost-savings arrangements. Such so-called savings may prove unfounded.

- Understand the surcharges and reinsurance fees that may be associated with the plan. These fees can add up, so it’s important to be aware of them before you choose a plan.

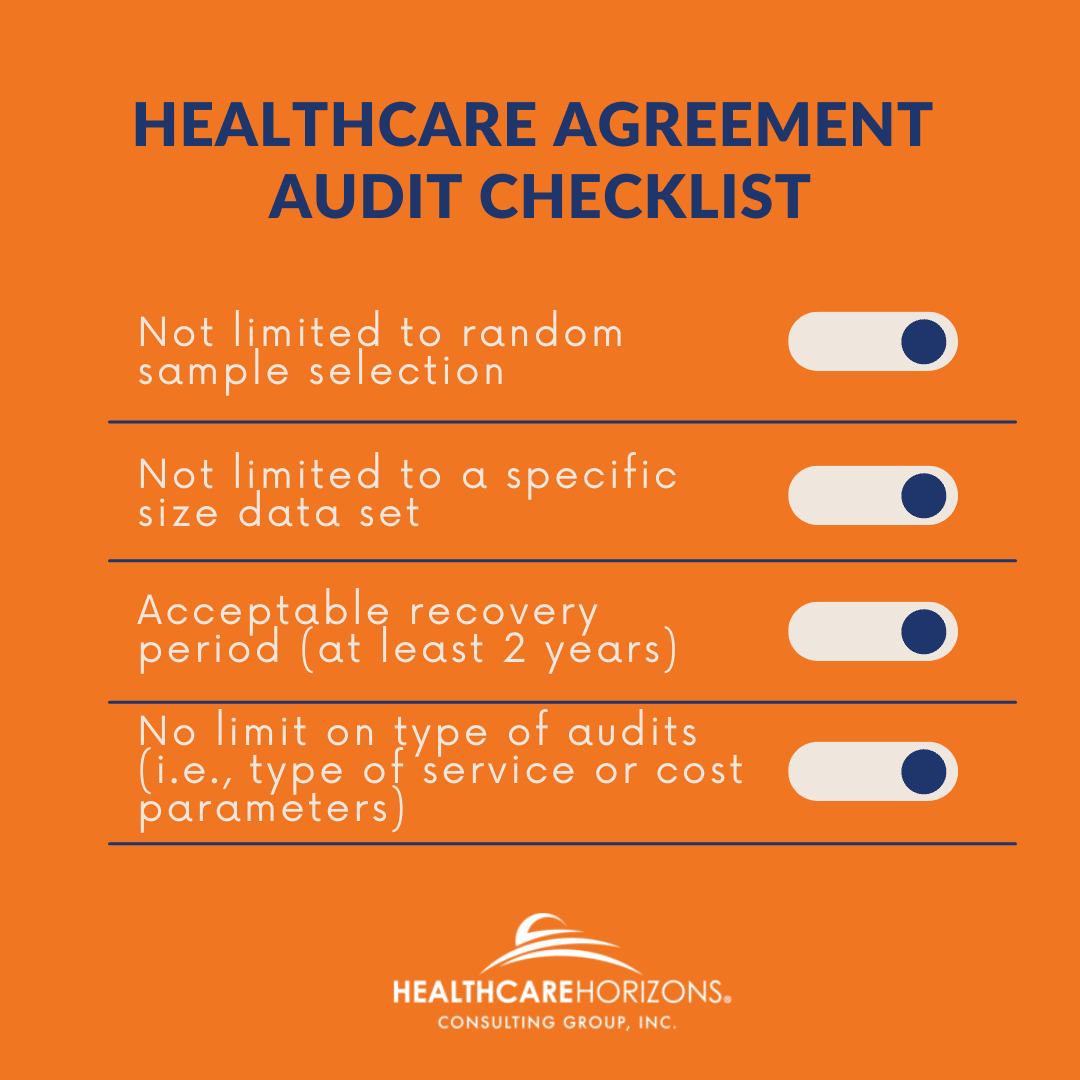

- Have a comprehensive audit performed annually by an independent company that has no conflicts of interest with any TPAs or insurance brokers.

Healthcare Horizons’ comprehensive medical claims audits identify overpaid claims and uncover hidden fees. In addition, we offer complimentary reviews of your third-party administrative services agreement audit rights language to ensure you aren’t restricted to a random sample audit. Let us help you uncover hidden fees and undisclosed costs before they hit your bottom line.