We talk a lot about WHY you should be getting external healthcare claims audits. (These statistics emphasize the importance.) So, in this article, we are going to assume you have made the excellent decision to have audits. Congratulations! But did you know that all audits aren’t created equal? Do not assume that your self-insured healthcare plan’s audit rights are covered by the TPAs standard language. These are the top two questions you need to ask your TPA to make sure you are not paying for a less-than-thorough audit.

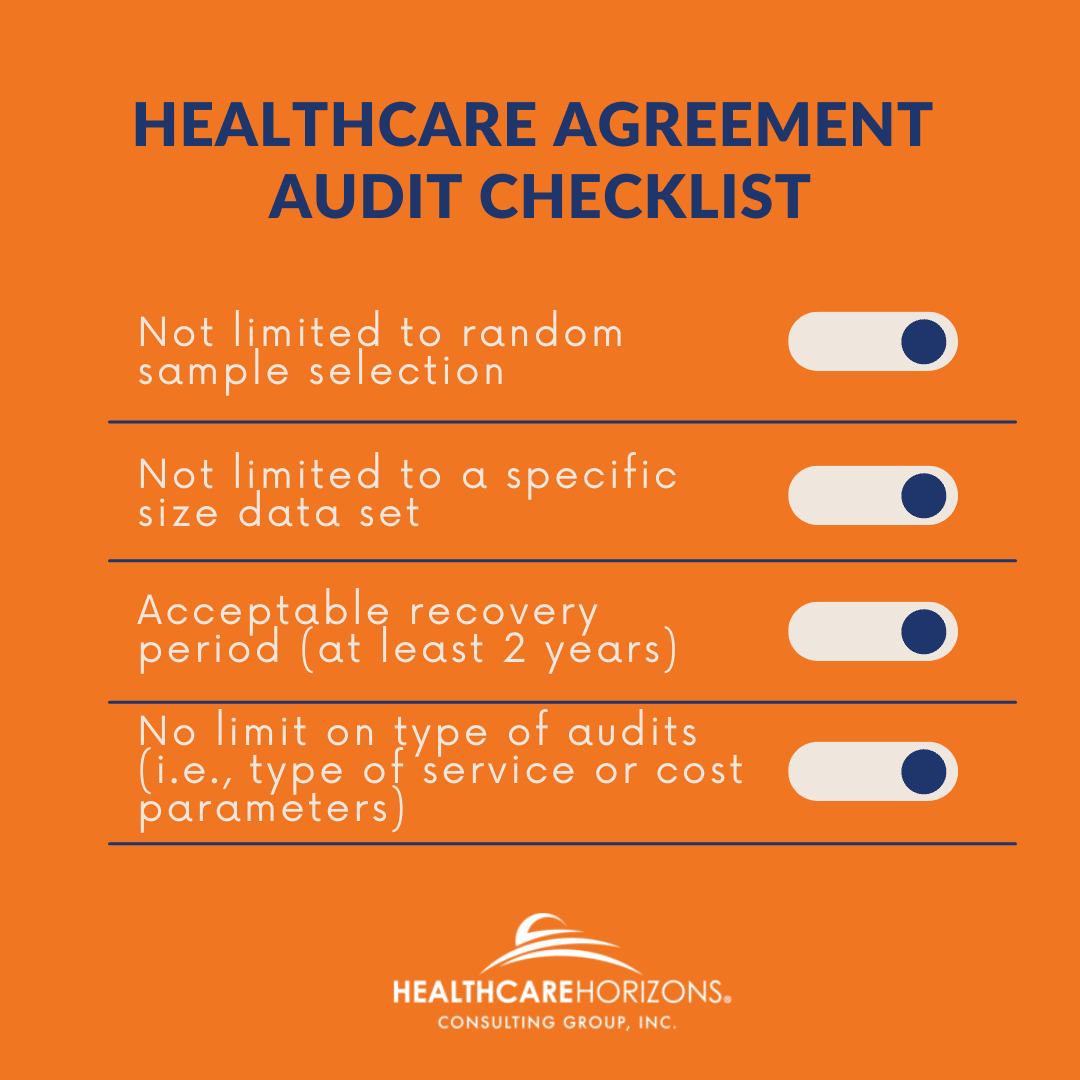

1. Do you allow for full 100% comprehensive auditing, without restricting the audit to random sample selection?

TPAs are entrusted by clients to manage the claims and payments of the plan, but their money is not at stake – yours is. Your company deserves the same protection a TPA would require for their own fully-funded plan.

There are two primary types of audits: random sample and comprehensive. Insist on comprehensive audits.

The typical outdated methodology for medical claims auditing is random sample selection. In this type of audit, auditors randomly select 200-300 claims out of millions of transactions. Auditors examine those claims for errors based on predetermined criteria and extrapolate the results to determine a claims error percentage of the entire data set. This approach historically has been considered standard practice when handling a large number of claims, but it carries a high margin of error that can work against the company in three ways.

- If the auditor encounters an error on a randomly selected sample claim, it is virtually impossible to determine if the error is isolated or systemic in nature.

- It is likely that significant one-off errors exist outside of the random sample selection.

- It is often difficult to convince payers to issue settlements based on the results of a random-sample audit.

We are different because of our comprehensive auditing process. We review every healthcare claim and Healthcare Horizons leadership submits a specifically targeted selection of claims to review onsite with the carrier. Our approach yields much better results because we identify both isolated and systemic errors and assign actual dollar impact to those errors, making a much stronger case to the payer.

If you are settling for a random sample selection audit, you are throwing money away. Unfortunately, many TPAs only want to allow random sample selection audits. They know the likelihood of any error being found using this method is much smaller. When comprehensive audits look at every claim, data errors will be found. But finding mistakes is a GOOD THING – for you. Insist on comprehensive audits.

2. Do you limit the number of audits that can be performed?

Service agreement audit language may contain many stipulations. A common restriction is on the number of audits conducted over a set length of time. Much like restricting audits to random sample selection, restricting audit frequency significantly limits the potential for errors to be discovered. Therefore, your ability to recover overpaid dollars is also greatly reduced.

Service agreements should not limit the number of times you can request healthcare claims audits. We recommend annual audits, not every other year as many TPAs enforce. One of the reasons that annual audits are so important is that claim recoveries are subject to time limits. It is common for the service agreement language to restrict claims recovery to two years or less. Here is the basic problem: when audits are not performed each year, claims may be too old to recover.

For example, in 2022 we can look back at the 2021 claims dataset for errors. If the audit is not performed until 2023, these 2021 claims will be too old to recover. If you are not having regular audits and a claim falls out of the timeline eligible for review, you will be out the dollars overpaid.

For our largest clients, we may audit quarterly, but annual reviews protect self-funded companies and their employees from overpayments and out-of-pocket expenses. In addition, our auditors are there to improve processes by providing suggestions and identifying inconsistencies, which will help eliminate overpayments and systemic errors.

The Top Two Questions Make the Difference

Now you know the top two questions to ask your TPA to ensure you are receiving the fullest scope of audit rights. Your next step is to work with someone that understands your rights, can execute a comprehensive audit, and return the most money to your bottom line.

In our 23 years of providing comprehensive healthcare claims audits, we have seen virtually every benefit setup, provider contract method, and claims administration policy that one would expect on claims audits of the world’s largest self-insured employers. Because of this experience, we quickly assess gaps in the healthcare audit rights in your service agreement. We offer a free audit rights assessment to make sure the audit language in your service agreement is not limiting your ability to recover funds. It is YOUR data and, more importantly, YOUR money. Don’t leave it on the table!